What Documents Are Needed To Buy A Home?

Buy a Home Michael Mastronardi May 20, 2026

Buy a Home Michael Mastronardi May 20, 2026

Buying a home is exciting, but the paperwork involved can feel overwhelming without proper preparation. From mortgage applications and financial verification to property documents and closing paperwork, understanding what lenders and real estate professionals require ahead of time can make the home buying process significantly smoother.

Whether purchasing a first home, relocating, or upgrading into a new property, buyers throughout Fairfield County, New Haven County, and communities across Connecticut can benefit from understanding which documents are needed before beginning the process.

Preparation not only reduces stress — it can also help avoid delays, strengthen offers, and improve overall confidence during the transaction.

Mortgage lenders and real estate professionals rely on documentation to verify financial stability, identity, purchasing power, and property eligibility. Missing paperwork, outdated records, or inconsistent information can delay underwriting, financing approval, and even closing timelines.

Having organized documentation early in the process helps:

Today’s Connecticut real estate market can move quickly, especially in competitive Fairfield County and New Haven County communities. Buyers who are financially prepared often position themselves more competitively when the right property becomes available.

Several foundational documents are required during nearly every home purchase transaction.

These commonly include:

Lenders use these records to evaluate financial stability, loan eligibility, and repayment capability.

It is also important to ensure:

Even small inconsistencies can slow down mortgage approval.

Mortgage lenders carefully review financial records to determine loan qualification and risk level.

Common financial documents include:

For self-employed buyers, additional documentation may include:

Stable income history and responsible financial management can improve both loan approval odds and financing terms.

Once a property is selected, buyers will also encounter important property-related documentation.

These may include:

Reviewing these documents carefully helps ensure the property is legally transferable, financially sound, and free from major unexpected issues.

A knowledgeable Connecticut real estate advisor can help explain these documents and identify potential concerns before closing.

Not every buyer situation is identical. Certain financing types or personal circumstances may require additional paperwork.

Examples include:

Buyers relocating from outside Connecticut or purchasing investment properties may also face additional lending requirements.

Preparing these documents early can help prevent unnecessary underwriting delays.

One of the most common reasons home purchases become delayed is incomplete or inconsistent documentation.

Common issues include:

Organization matters throughout the mortgage process.

Creating a dedicated folder with digital and printed copies of important records can make communication with lenders, attorneys, and agents significantly easier.

Pre-approval is one of the most important early steps in the home buying process.

A mortgage pre-approval helps buyers:

In competitive Connecticut real estate markets, many sellers prioritize buyers who already have financing in place.

Preparation can often become a competitive advantage.

Buying a home involves much more than simply finding the right property. Financial preparation, organized documentation, and understanding the mortgage process all play important roles in creating a successful transaction.

When buyers prepare early, communicate clearly, and stay organized, the process becomes far less stressful and significantly more manageable.

Whether purchasing in Fairfield County, New Haven County, or surrounding Connecticut communities, understanding the required documents ahead of time can help buyers move through the process with greater confidence and clarity.

Most lenders require identification, proof of income, bank statements, tax returns, employment verification, and authorization to review your credit history.

Most mortgage lenders request between 2 and 6 months of bank statements depending on the loan type and financial profile.

Yes. Self-employed buyers often need business tax returns, profit and loss statements, 1099 forms, and additional income verification documentation.

Credit reports help lenders evaluate payment history, debt management, financial risk, and overall loan eligibility.

Yes. Missing or inconsistent documentation can delay underwriting, financing approval, and final closing timelines.

Buying a home becomes significantly easier when the right guidance and preparation are in place from the beginning. Michael Mastronardi helps buyers throughout Fairfield County, New Haven County, and communities across Connecticut navigate the home buying process with clear communication, strategic guidance, and local market expertise.

Whether preparing for pre-approval, searching for the right home, or navigating inspections and closing, expert support can make the entire process smoother and far less stressful.

Stay up to date on the latest real estate trends.

Why online home value estimates can be helpful starting points—but often miss the factors that truly determine what a home is worth.

Will home prices rise? Will inventory improve? Here's what buyers and sellers should expect in the Connecticut housing market in 2026.

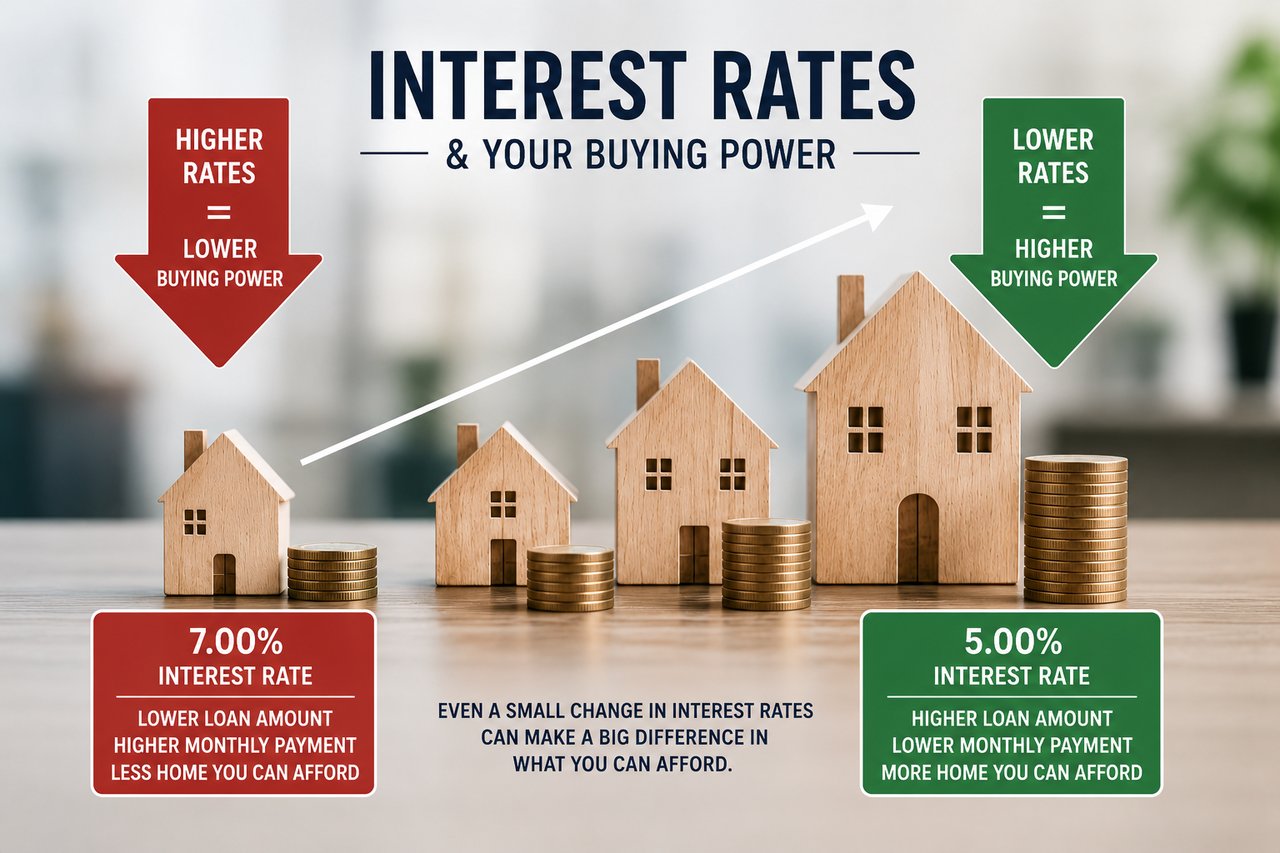

Interest Rates

Understanding how mortgage rates affect affordability, monthly payments, and buying power in today's Connecticut housing market.

Connecticut Real Estate

Discover the Connecticut communities that offer the ideal balance of commute time, lifestyle, schools, and quality of life for New York City professionals.

Buy a Home

Buying a home feels exciting. It is a big life step and often a dream for many people. But the process can feel confusing when paperwork starts piling up. The good new… Read more

Condo vs Single Family Home

Understanding the differences in cost, maintenance, lifestyle, privacy, and long-term value before buying in Connecticut.

Home Buying Process

Understanding the Connecticut home buying process from budgeting and pre-approval to inspections, financing, and closing day.

First Time Home Buyer

A practical guide for first-time buyers navigating budgeting, credit, loan programs, and affordable homeownership opportunities in Fairfield County and beyond.

Townhouse vs Apartment

A complete guide to comparing townhouses and apartments in Fairfield County, including cost, privacy, maintenance, and long-term value.