How Interest Rates Impact Home Buying in Connecticut (2026 Guide)

Interest Rates June 8, 2026

Interest Rates June 8, 2026

Buying a home is one of the largest financial decisions most people will ever make. While buyers often focus on home prices, one factor can dramatically impact affordability even when prices remain unchanged: mortgage interest rates.

In Connecticut's housing market, understanding how interest rates affect your buying power can help you make smarter decisions and avoid surprises during the home-buying process.

When you finance a home purchase, you're borrowing money from a lender and repaying it over time with interest.

The interest rate determines how much you'll pay to borrow that money.

Even small changes in mortgage rates can significantly impact:

Monthly mortgage payments

Total purchasing power

Loan approval amounts

Long-term housing costs

For many buyers, interest rates influence affordability just as much as the actual purchase price.

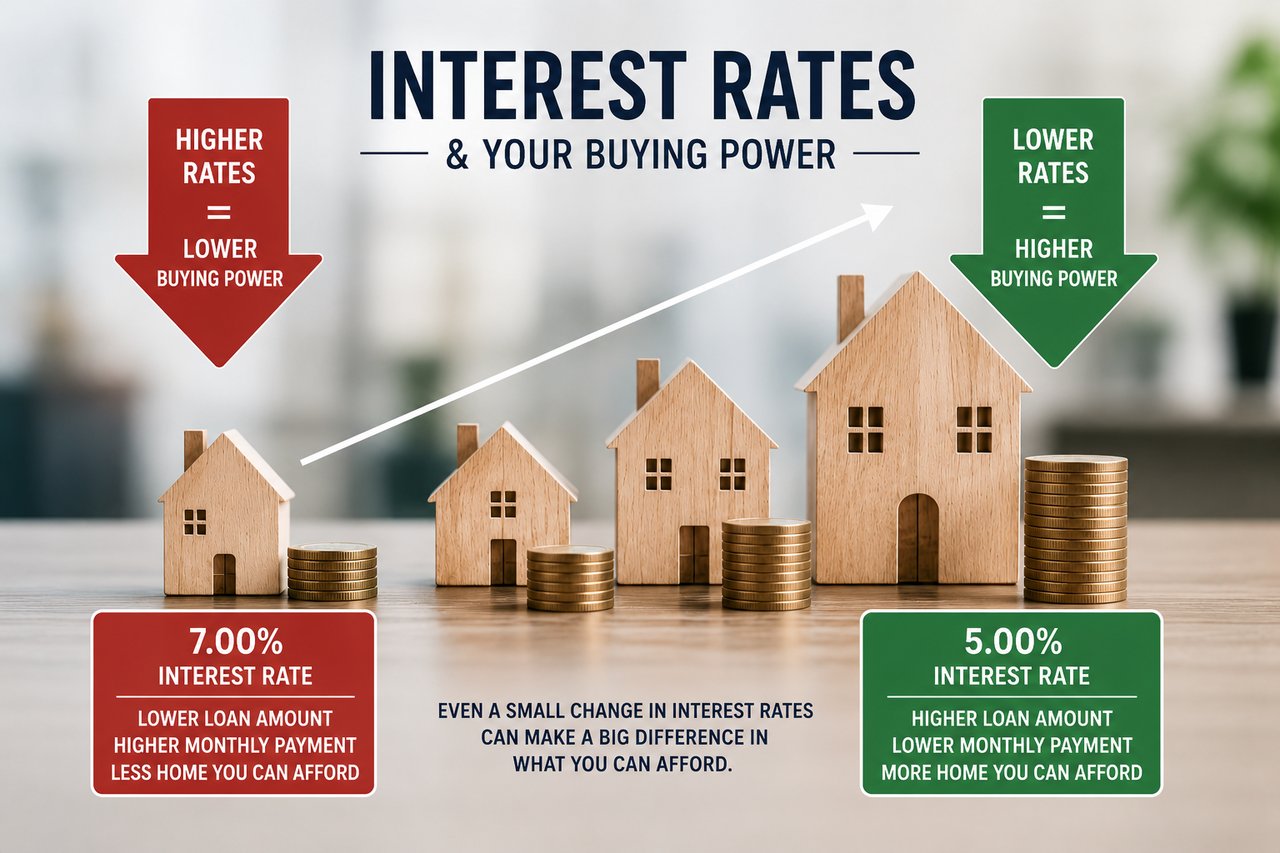

One of the biggest impacts of rising interest rates is reduced purchasing power.

As rates increase, monthly payments rise. Because lenders evaluate your debt-to-income ratio when approving a mortgage, higher payments often mean qualifying for a smaller loan amount.

For example, a buyer who qualified for a $700,000 home at one interest rate may only qualify for a $625,000 home after rates increase.

This can affect which towns, neighborhoods, or property types fit within your budget.

Many buyers focus primarily on purchase price, but monthly affordability often matters more.

A difference of just one percentage point in interest rate can increase monthly payments by hundreds of dollars over the life of a mortgage.

This is why it's important to evaluate:

Principal and interest

Property taxes

Homeowners insurance

Maintenance costs

HOA fees, if applicable

The goal is finding a payment that comfortably fits your lifestyle and financial goals.

Mortgage rates don't just impact individual buyers—they influence the broader housing market as well.

When rates rise:

Some buyers pause their search

Demand may soften

Homes can take longer to sell

Competition may decrease

When rates fall:

More buyers enter the market

Competition often increases

Multiple-offer situations become more common

Home prices may experience upward pressure

The relationship isn't always immediate, but rates play a major role in market activity.

This is one of the most common questions buyers ask.

The truth is that trying to perfectly time interest rates can be difficult.

While lower rates improve affordability, they can also increase buyer competition and push prices higher.

Many buyers find that purchasing the right home when they're financially prepared is more important than waiting for the "perfect" rate environment.

Remember, while home prices are permanent, mortgage rates can often be refinanced if conditions improve.

While buyers cannot control mortgage rates, they can take steps to strengthen their financial position.

Higher credit scores often qualify for more favorable mortgage terms and lower interest rates.

Lower debt can improve your debt-to-income ratio and increase purchasing power.

A larger down payment may reduce monthly costs and improve financing options.

Pre-approval provides a clear understanding of your budget before you begin shopping.

Large purchases before applying for a mortgage can impact your debt-to-income ratio and potentially affect loan approval.

When mortgage rates rise, some buyers wonder whether renting makes more sense.

The answer depends on your financial goals, timeline, and overall housing needs.

Renting may offer:

However, renting does not build equity or provide long-term ownership benefits.

Buying a home can offer:

While higher interest rates may impact affordability, they don't automatically make renting the better choice. Many buyers choose to purchase when they're financially ready and refinance later if rates improve.

Renting

Buying

The best choice depends on your personal finances, future plans, and lifestyle goals.

Yes. Higher mortgage rates increase monthly payments, which often reduces the loan amount a buyer qualifies for. Lower rates typically increase purchasing power.

There is no perfect answer. Lower rates improve affordability, but they can also increase competition among buyers. The best time to buy is often when your personal finances and housing goals align.

In many cases, yes. Homeowners may have the option to refinance their mortgage if rates become more favorable in the future.

Both matter. A lower purchase price can help affordability, but even small changes in mortgage rates can significantly impact monthly payments over time.

Interest rates are one of the most important factors influencing home affordability in today's market.

Higher rates can reduce purchasing power and increase monthly payments, while lower rates often improve affordability and expand buying options.

The good news is that buyers have more control than they may realize. Improving credit, reducing debt, building savings, and obtaining pre-approval can all strengthen your position regardless of market conditions.

Rather than focusing solely on interest rates, successful buyers often focus on creating a strategy that aligns with their financial goals, lifestyle needs, and long-term plans.

Whether you're purchasing your first home, relocating from New York, or exploring your next move, understanding today's market is essential.

If you're considering buying in Fairfield County or New Haven County, I'd be happy to help you evaluate your options, understand your purchasing power, and create a strategy that aligns with your goals.

• What Credit Score Do You Need to Buy a Home in Connecticut?

• Hidden Costs of Buying a Home in Connecticut

• How Much House Can You Afford in Connecticut?

• Best Connecticut Towns for NYC Commuters

Michael Mastronardi is a Connecticut Real Estate Advisor serving buyers and sellers throughout Fairfield County and New Haven County. He helps clients navigate the housing market with local expertise, strategic guidance, and a commitment to exceptional service.

Stay up to date on the latest real estate trends.

Why online home value estimates can be helpful starting points—but often miss the factors that truly determine what a home is worth.

Will home prices rise? Will inventory improve? Here's what buyers and sellers should expect in the Connecticut housing market in 2026.

Interest Rates

Understanding how mortgage rates affect affordability, monthly payments, and buying power in today's Connecticut housing market.

Connecticut Real Estate

Discover the Connecticut communities that offer the ideal balance of commute time, lifestyle, schools, and quality of life for New York City professionals.

Buy a Home

Buying a home feels exciting. It is a big life step and often a dream for many people. But the process can feel confusing when paperwork starts piling up. The good new… Read more

Condo vs Single Family Home

Understanding the differences in cost, maintenance, lifestyle, privacy, and long-term value before buying in Connecticut.

Home Buying Process

Understanding the Connecticut home buying process from budgeting and pre-approval to inspections, financing, and closing day.

First Time Home Buyer

A practical guide for first-time buyers navigating budgeting, credit, loan programs, and affordable homeownership opportunities in Fairfield County and beyond.

Townhouse vs Apartment

A complete guide to comparing townhouses and apartments in Fairfield County, including cost, privacy, maintenance, and long-term value.