Fixed vs Variable Rate Mortgages in Connecticut: Which Is Right for You?

Mortgage Rates Michael Mastronardi April 8, 2026

Mortgage Rates Michael Mastronardi April 8, 2026

Compare fixed vs variable rate mortgages in Connecticut. Learn how interest rates, risk, and long-term plans impact your home financing decision.

Choosing the right mortgage is one of the most important financial decisions you’ll make when buying a home.

Two of the most common options are:

Each offers different advantages depending on your financial goals, risk tolerance, and long-term plans.

Understanding how they work can help you make a more confident and informed decision.

A fixed-rate mortgage means your interest rate remains the same for the entire term of the loan.

This type of loan is often preferred by buyers who value stability and consistency.

A variable-rate mortgage (also known as an adjustable-rate mortgage or ARM) has an interest rate that can change over time based on market conditions.

This option can be attractive for buyers who plan to sell or refinance within a shorter time frame.

| Feature | Fixed-Rate Mortgage | Variable-Rate Mortgage |

|---|---|---|

| Interest Rate | Remains constant | Adjusts over time |

| Monthly Payment | Predictable | Can fluctuate |

| Risk Level | Low | Moderate to higher |

| Budgeting | Simple | Requires flexibility |

| Best For | Long-term ownership | Short-term strategies |

Fixed-rate mortgages are often the most straightforward option.

They provide:

This is especially valuable in environments where interest rates may rise.

Variable-rate mortgages can offer advantages in certain situations.

They may be a good fit if you:

However, it’s important to understand the potential for increased payments over time.

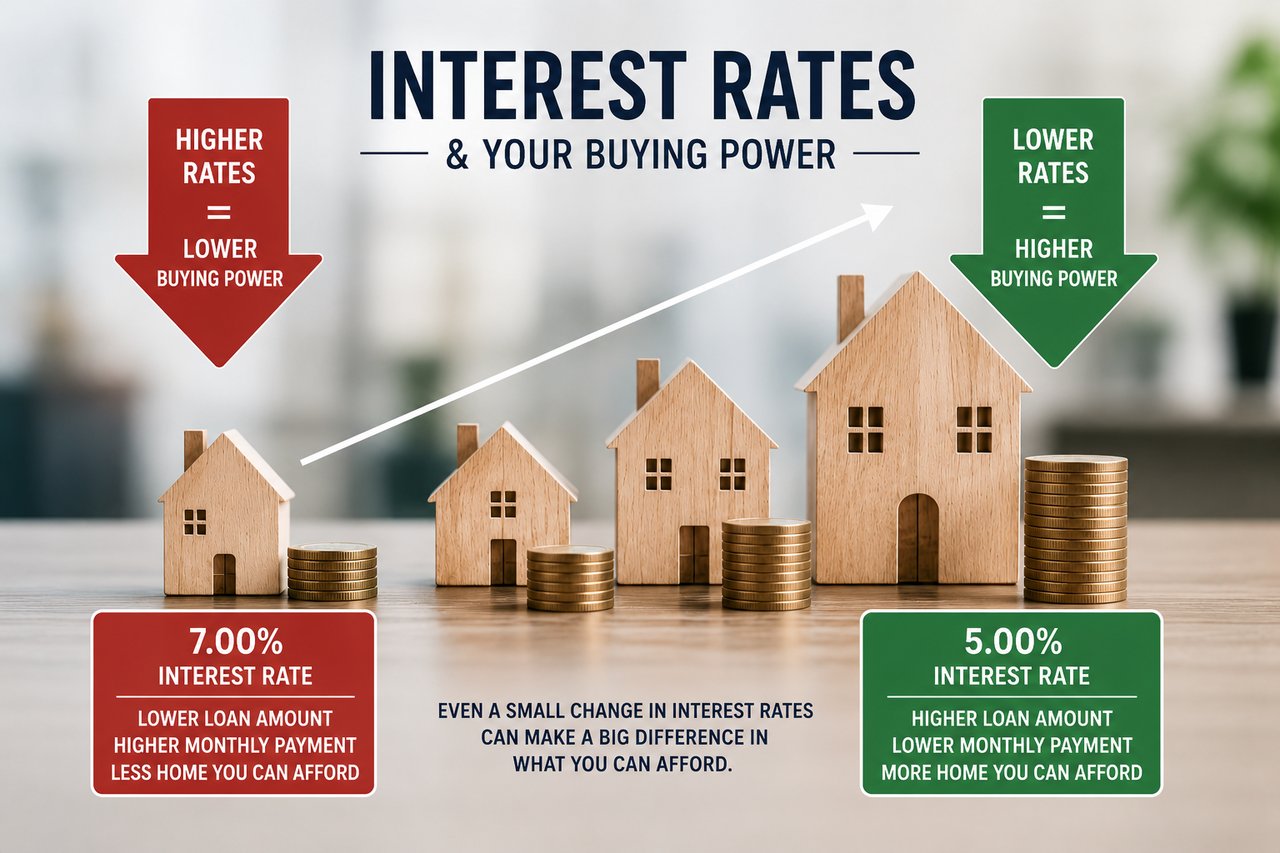

Interest rates are influenced by broader economic trends, including inflation and Federal Reserve policy.

Before choosing a mortgage, it’s important to:

Buyers who align their financing with market conditions often make more strategic decisions.

When comparing mortgage options, avoid:

A mortgage should align with both your current situation and future plans.

Your mortgage choice directly affects:

Understanding your financing options is just one part of the equation. For more insight, you can also review:

• How Much House Can You Afford in Connecticut (2026 Guide)

• What Credit Score Do You Need to Buy a Home in Connecticut

There is no one-size-fits-all answer.

A fixed-rate mortgage may be best if you:

A variable-rate mortgage may be a fit if you:

The right choice depends on your goals, timeline, and financial profile.

Mortgage decisions don’t happen in isolation—they are part of a broader home buying strategy.

Working with a knowledgeable real estate advisor can help you evaluate both property and financing decisions together.

Michael Mastronardi is a Connecticut real estate advisor serving buyers and sellers across Fairfield County and New Haven County, providing guidance grounded in local market knowledge and a strategic approach to real estate.

• How Much House Can You Afford in Connecticut (2026 Guide)

• What Credit Score Do You Need to Buy a Home in Connecticut

• Hidden Costs of Buying a Home in Connecticut (2026 Guide)

• Best Connecticut Towns for NYC Commuters (2026 Guide)

Stay up to date on the latest real estate trends.

Why online home value estimates can be helpful starting points—but often miss the factors that truly determine what a home is worth.

Will home prices rise? Will inventory improve? Here's what buyers and sellers should expect in the Connecticut housing market in 2026.

Interest Rates

Understanding how mortgage rates affect affordability, monthly payments, and buying power in today's Connecticut housing market.

Connecticut Real Estate

Discover the Connecticut communities that offer the ideal balance of commute time, lifestyle, schools, and quality of life for New York City professionals.

Buy a Home

Buying a home feels exciting. It is a big life step and often a dream for many people. But the process can feel confusing when paperwork starts piling up. The good new… Read more

Condo vs Single Family Home

Understanding the differences in cost, maintenance, lifestyle, privacy, and long-term value before buying in Connecticut.

Home Buying Process

Understanding the Connecticut home buying process from budgeting and pre-approval to inspections, financing, and closing day.

First Time Home Buyer

A practical guide for first-time buyers navigating budgeting, credit, loan programs, and affordable homeownership opportunities in Fairfield County and beyond.

Townhouse vs Apartment

A complete guide to comparing townhouses and apartments in Fairfield County, including cost, privacy, maintenance, and long-term value.