What Credit Score Do You Need to Buy a Home in Connecticut?

Credit Score Michael Mastronardi April 11, 2026

Credit Score Michael Mastronardi April 11, 2026

Learn what credit score you need to buy a home in Connecticut, how it impacts mortgage rates, and how to improve your buying position.

Buying a home is one of the most important financial decisions you’ll make—and your credit score plays a major role in that process.

Your credit score helps lenders determine:

While there is no single “perfect” number, understanding how credit works can help you prepare and move forward with confidence.

Different loan programs have different credit score requirements. Knowing these ranges early helps you plan effectively and avoid delays during the home buying process.

Higher credit scores generally unlock better rates and more favorable loan terms.

Your credit score is a key factor lenders use to evaluate risk.

It directly impacts:

Even a small increase in your score can result in meaningful long-term savings.

Credit scores fall into general ranges:

Most buyers aim for at least a 620–680+ range to access stronger financing options.

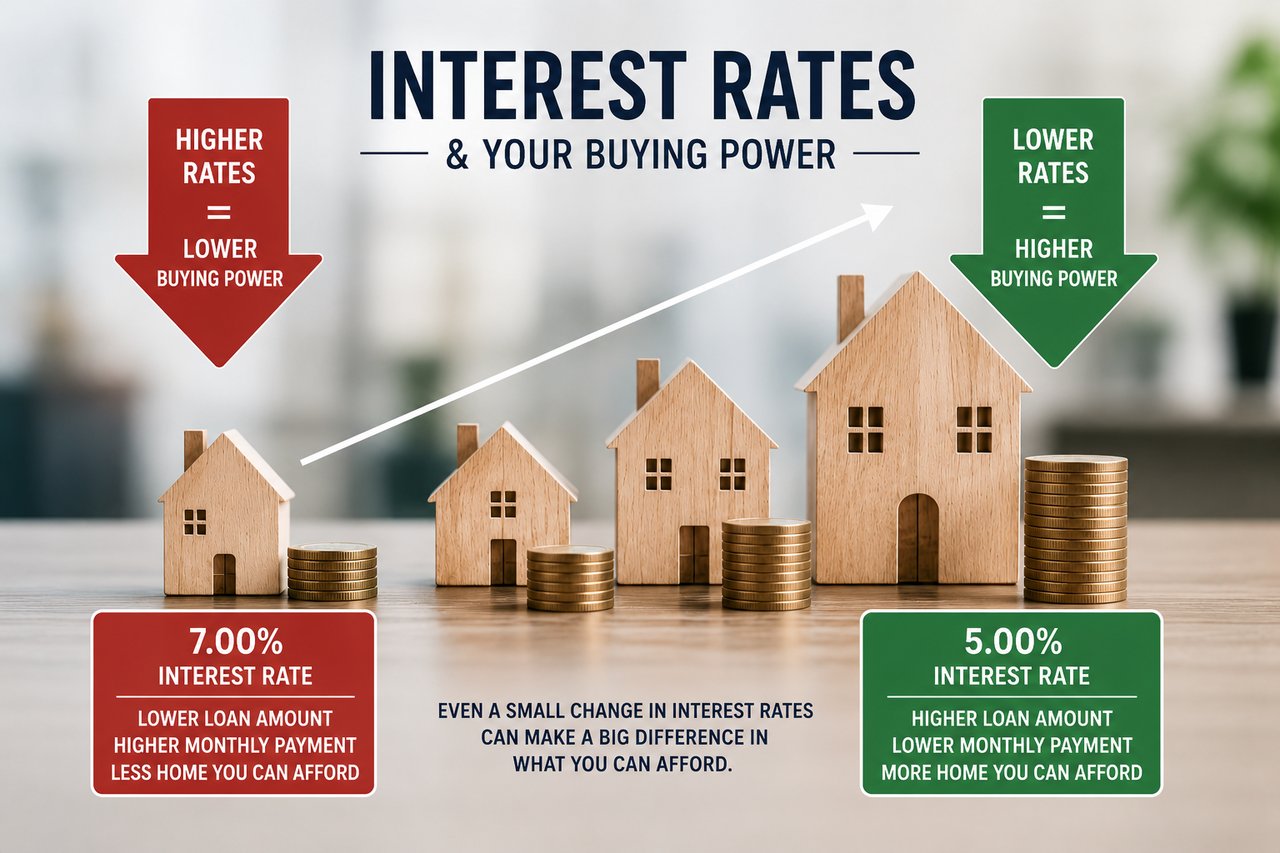

Your credit score plays a major role in determining your mortgage interest rate.

Over time, this difference can add up to tens of thousands of dollars.

Yes - buying a home with a lower credit score is still possible.

Options may include:

However, improving your credit score before buying can significantly improve your financing terms.

Preparing your credit profile in advance can strengthen your position.

Focus on:

Even modest improvements can increase your buying power.

Certain actions can quickly lower your credit score:

Avoiding these mistakes helps maintain a stronger financial profile.

While your credit score is important, lenders evaluate your full financial picture, including:

A strong overall profile can help offset minor credit challenges.

If you're buying your first home, preparation is key.

Clarity early in the process leads to better decisions later.

Timing your application matters.

It’s best to apply when:

Preparation helps ensure a smoother transaction.

Most buyers need at least a 580–620 credit score, depending on the loan type. Higher scores provide better rates and terms.

Yes, options like FHA loans allow lower scores, but improving your credit can lead to better financing.

Paying down balances, making on-time payments, and correcting errors on your credit report can help improve your score over time.

No. Each loan program has different requirements, which is why exploring multiple options is important.

Yes. A higher score typically results in lower interest rates and reduced overall borrowing costs.

Understanding your credit score is one of the first steps toward buying a home successfully.

With the right preparation and guidance, you can position yourself for better financing, stronger offers, and a smoother overall experience.

Michael Mastronardi is a Connecticut real estate advisor serving buyers and sellers across Fairfield County and New Haven County, helping clients navigate the market with local insight and strategic guidance.

• How Much House Can You Afford in Connecticut (2026 Guide)

• Hidden Costs of Buying a Home in Connecticut (2026 Guide)

• Best Connecticut Towns for NYC Commuters (2026 Guide)

Stay up to date on the latest real estate trends.

Why online home value estimates can be helpful starting points—but often miss the factors that truly determine what a home is worth.

Will home prices rise? Will inventory improve? Here's what buyers and sellers should expect in the Connecticut housing market in 2026.

Interest Rates

Understanding how mortgage rates affect affordability, monthly payments, and buying power in today's Connecticut housing market.

Connecticut Real Estate

Discover the Connecticut communities that offer the ideal balance of commute time, lifestyle, schools, and quality of life for New York City professionals.

Buy a Home

Buying a home feels exciting. It is a big life step and often a dream for many people. But the process can feel confusing when paperwork starts piling up. The good new… Read more

Condo vs Single Family Home

Understanding the differences in cost, maintenance, lifestyle, privacy, and long-term value before buying in Connecticut.

Home Buying Process

Understanding the Connecticut home buying process from budgeting and pre-approval to inspections, financing, and closing day.

First Time Home Buyer

A practical guide for first-time buyers navigating budgeting, credit, loan programs, and affordable homeownership opportunities in Fairfield County and beyond.

Townhouse vs Apartment

A complete guide to comparing townhouses and apartments in Fairfield County, including cost, privacy, maintenance, and long-term value.