Renting vs. Buying: Which Makes More Financial Sense?

Renting vs. buying Michael Mastronardi March 12, 2026

Renting vs. buying Michael Mastronardi March 12, 2026

Deciding between renting and buying a home can feel tricky. Renting is easier at first. Less money upfront and fewer responsibilities. But paying rent every month doesn’t build your own money. Buying takes more money first, like a down payment and fees, but you own something that can grow in value. If you plan to stay long and want to build wealth, buying usually makes more financial sense. Renting is good if you need flexibility or move a lot.

Renting is simple. You usually pay a security deposit and maybe first and last month’s rent. That’s it. Most people can manage that.

Buying costs more at the start. You need a down payment, closing costs, inspection fees, and insurance.

Here’s a quick look at upfront costs:

Renting: Deposit plus first month’s rent. Usually 1–2 months total.

Buying: Down payment (5–20% of home price), closing costs ($5,000–$15,000), inspection, and insurance.

Buying is more expensive upfront, but it’s an investment. Renting keeps money free for other things, but it doesn’t grow your wealth.

Renting is easy to plan. You pay the same rent each month. Sometimes utilities are included. Repairs are usually handled by the landlord.

Buying has more bills. Mortgage, property taxes, insurance, utilities, and repairs. Payments can go up if taxes increase or something breaks.

Here’s a simple comparison:

Renting: Rent is fixed, utilities sometimes included, and the landlord fixes things.

Buying: Mortgage, taxes, insurance, utilities, repairs, and possible HOA fees.

Owning a home may cost more each month, but it builds equity. Renting may feel cheaper, but it doesn’t give you an asset.

Equity means your share of the house you actually own. Each mortgage payment grows your equity. Over time, the home can rise in value. When you sell, you might make money.

Renting does not build equity. Rent money goes away each month. You have flexibility, but no investment.

Buying: Builds wealth over time through equity and possible property growth.

Renting: Offers freedom, low responsibility, but no return on money.

Buying also has tax benefits. Mortgage interest and property taxes can sometimes be deducted. This can save money and make owning a home more financially smart.

Renting gives freedom. If your job moves or life changes, you can leave at the end of the lease.

Buying ties you to a home. Selling a house takes time and planning. You can’t move as quickly.

Renting: Good for short-term living, frequent moves, or uncertain plans.

Buying: Better for long-term stability and staying in one place.

Flexibility comes at a cost. Renting is easy, but it doesn’t create wealth. Buying costs more freedom but gives stability and financial benefits.

Renting relieves responsibility. Landlords fix broken things. You just pay rent and enjoy your home.

Owning a home means you handle repairs. Roof, plumbing, heating, and appliances are your responsibility. Costs can be small or very large, depending on the home.

Renting: The landlord fixes problems. Predictable monthly cost.

Buying: You fix everything. Costs can be big or small.

Owning teaches money management and planning. Renting avoids surprise expenses.

Buying a home can be a smart financial choice for people who are ready to commit and want to make their money work for them over time. Consider the following situations when buying usually makes more sense:

Buying is smart if you:

Plan to stay 5–7 years or longer

Have savings for a down payment and closing costs

Want to build equity and long-term wealth

Prefer stability over moving frequently

If the market is strong and interest rates are reasonable, buying can be a great financial move.

Renting can be the smarter choice for people who need flexibility or aren’t ready for the costs and responsibilities of owning a home. Consider renting if any of the following situations apply:

Renting may be better if you:

Move often for work, school, or lifestyle

Don’t have savings for a down payment

Want low responsibility

Prefer short-term living without tying up cash

Renting keeps money free for other things but does not create property equity.

Q. Is buying cheaper than renting?

Buying a home usually costs more upfront because of the down payment, closing fees, and ongoing bills like taxes and insurance. Renting is cheaper in the short term and predictable. Over time, buying can be financially better because mortgage payments build equity, and the home may increase in value.

Q. How long should I stay in a house to make buying worth it?

It’s best to stay in a home for about 5–7 years. This gives time to recover upfront costs, like down payment and closing fees, and benefit from property value growth. Shorter stays may make renting more practical because selling a home too soon can reduce financial gain.

Q. Can renting help me save for buying later?

Yes. Renting usually requires less money upfront, making it easier to save each month. By budgeting wisely while renting, you can build a down payment for a future home. This strategy allows you to prepare financially for buying without overextending yourself.

Q. What hidden costs should I expect when buying?

Buying a home comes with extra costs beyond the price. Expect property taxes, homeowners' insurance, routine maintenance, repairs, and sometimes HOA fees. These costs can add up fast, so planning helps avoid surprises and ensures your budget covers all expenses involved in homeownership.

Q. Does owning a home give other financial benefits?

Yes. Homeowners can often deduct mortgage interest and property taxes from their taxes. Plus, owning builds equity over time, and the home may increase in value. These benefits can make buying financially smarter than renting, giving long-term wealth growth and potential tax advantages.

Take action today and make your next move with confidence. Michael Mastronardi can help you explore homes for sale in Easton, CT and figure out whether renting or buying suits your budget, goals, and lifestyle. With expert guidance, clear advice, and local market knowledge, you can make a smart, informed decision. Call now to get personalized support and take the first step toward your future home.

Stay up to date on the latest real estate trends.

Why online home value estimates can be helpful starting points—but often miss the factors that truly determine what a home is worth.

Will home prices rise? Will inventory improve? Here's what buyers and sellers should expect in the Connecticut housing market in 2026.

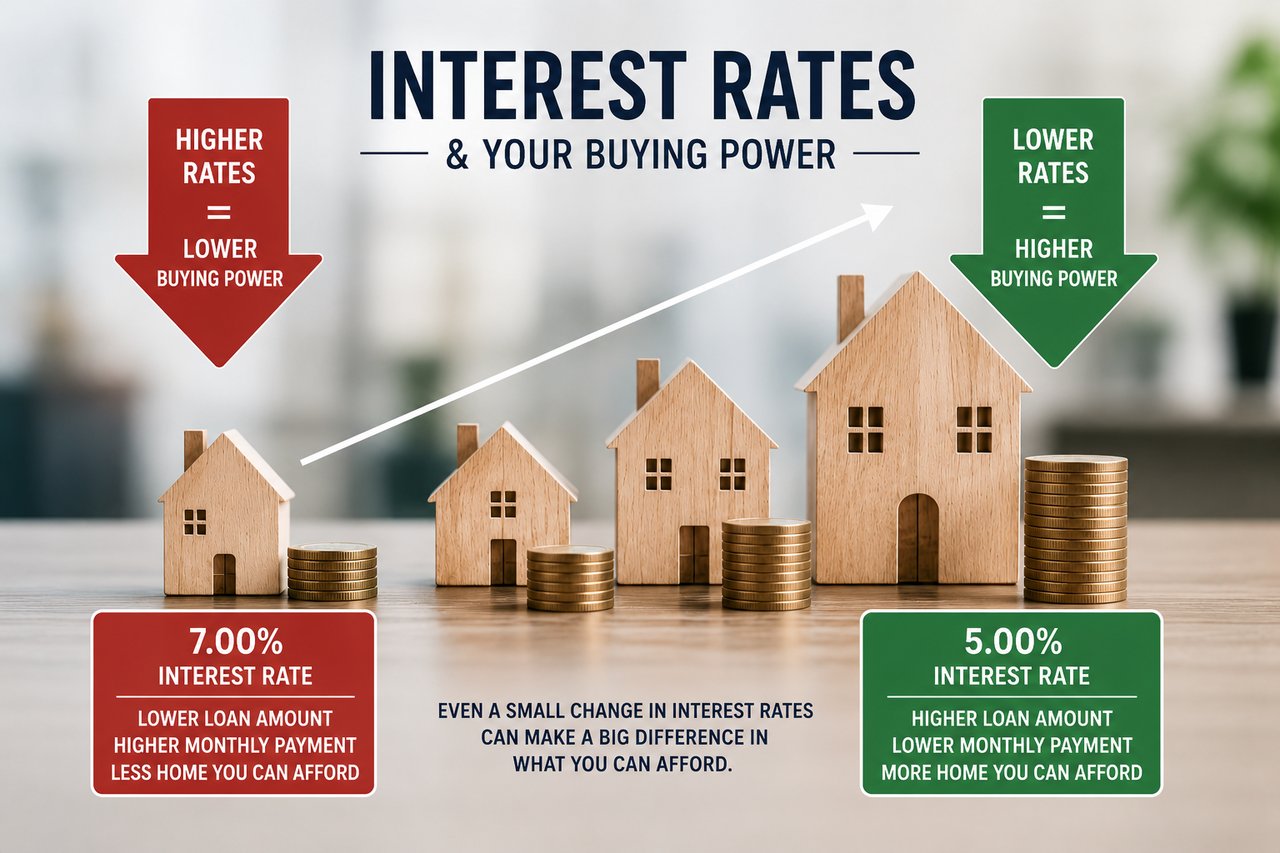

Interest Rates

Understanding how mortgage rates affect affordability, monthly payments, and buying power in today's Connecticut housing market.

Connecticut Real Estate

Discover the Connecticut communities that offer the ideal balance of commute time, lifestyle, schools, and quality of life for New York City professionals.

Buy a Home

Buying a home feels exciting. It is a big life step and often a dream for many people. But the process can feel confusing when paperwork starts piling up. The good new… Read more

Condo vs Single Family Home

Understanding the differences in cost, maintenance, lifestyle, privacy, and long-term value before buying in Connecticut.

Home Buying Process

Understanding the Connecticut home buying process from budgeting and pre-approval to inspections, financing, and closing day.

First Time Home Buyer

A practical guide for first-time buyers navigating budgeting, credit, loan programs, and affordable homeownership opportunities in Fairfield County and beyond.

Townhouse vs Apartment

A complete guide to comparing townhouses and apartments in Fairfield County, including cost, privacy, maintenance, and long-term value.